In the realm of digital innovation, few concepts have generated as much buzz and excitement as blockchain. Yet, for many, the term remains shrouded in mystery, with its true meaning and potential eluding grasp. So, what exactly is blockchain? In this blog post, we’ll provide a comprehensive definition of blockchain, unraveling its intricacies and exploring its transformative impact across industries.

Understanding Blockchain: The Basics

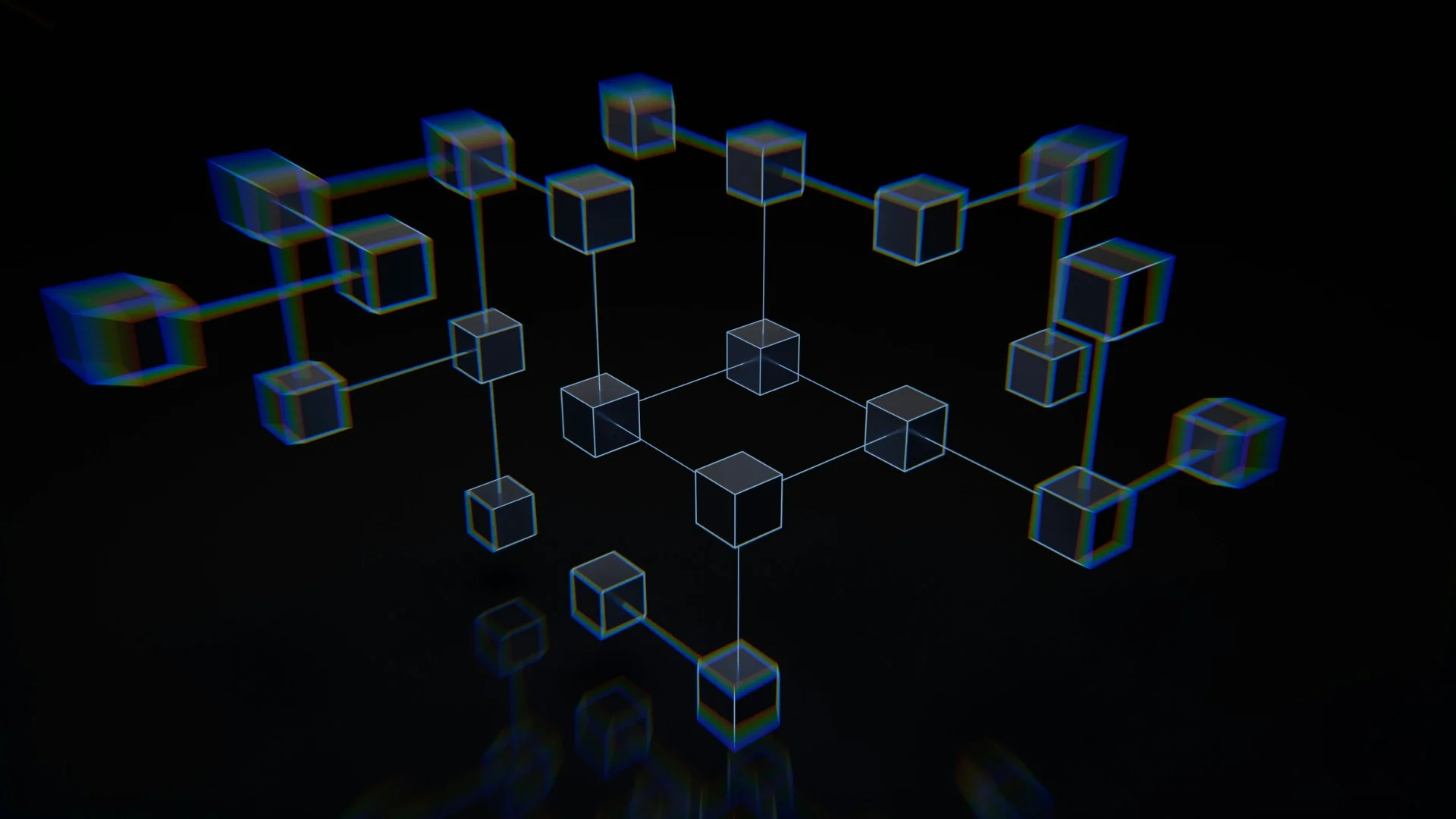

At its core, blockchain is a decentralized, distributed ledger technology that enables the secure and transparent recording of transactions across a network of computers. The term “blockchain” refers to the chain of blocks containing transactional data, cryptographically linked in a chronological sequence. Each block represents a set of transactions and is connected to the previous block through a cryptographic hash, forming an immutable chain.

Key Components of Blockchain:

- Blocks: Each block in the blockchain contains a batch of transactions, along with a cryptographic hash of the previous block, a timestamp, and other metadata.

- Cryptographic Hashes: Cryptographic hashes are unique, fixed-size strings generated by applying a mathematical algorithm to the data within a block. These hashes serve as digital fingerprints, ensuring the integrity and immutability of the blockchain.

- Decentralization: Blockchain operates on a decentralized network of nodes, with each participant maintaining a copy of the ledger. This decentralized architecture eliminates the need for a central authority and reduces the risk of single points of failure or manipulation.

- Consensus Mechanisms: Consensus mechanisms are protocols that enable network participants to agree on the validity of transactions and the addition of new blocks to the blockchain. Common consensus mechanisms include proof of work (PoW), proof of stake (PoS), and delegated proof of stake (DPoS).

Applications of Blockchain Technology:

Blockchain technology has far-reaching implications across industries, offering solutions to a wide range of challenges:

- Finance: Blockchain enables secure and transparent peer-to-peer transactions, remittances, and decentralized financial services such as lending, borrowing, and asset tokenization.

- Supply Chain Management: Blockchain enhances transparency and traceability in supply chains, combating counterfeit goods, ensuring ethical sourcing, and streamlining regulatory compliance.

- Healthcare: Blockchain facilitates secure and interoperable sharing of medical records, drug traceability, and clinical trial management, enhancing patient privacy and data integrity.

- Governance: Blockchain can be utilized for secure voting systems, transparent identity management, and immutable records of land ownership, promoting accountability and trust in government processes.

Conclusion: Unlocking the Potential of Blockchain

In conclusion, blockchain represents a paradigm shift in how data is stored, shared, and transacted in the digital age. Its decentralized, transparent, and immutable nature holds the promise of transforming industries, empowering individuals, and fostering trust in the global economy. As blockchain continues to evolve and mature, its impact will be felt across diverse sectors, driving innovation, efficiency, and inclusivity in the digital landscape. Whether you’re a developer, entrepreneur, or simply curious about the potential of blockchain, understanding its definition and underlying principles is the first step towards unlocking its transformative potential.

Leave a Reply